What is risk profiling?

The risk profiling process can assist you in determining your tolerance to risk and how that relates to particular investments and your broader financial plan. It is a process that professional advisors use to assess what the optimal level of risk is for their clients. It involves a mix of tools, including questionnaires, to provide an insight as to what level of volatility is right for you. The risk profiles are not a perfect science, but a starting point to assess where you sit in terms of comfort on the risk-return spectrum. The higher the perceived return from an investment, usually the greater the risk. On the flip side, the lower the return, the less your capital is at risk.

While important, a risk profile is not the only information you should consider before making an investment decision. These tools do not take into account your individual investment preferences, financial situation, objectives or other needs. These factors need to form part of the process for making investment decisions and are the reason good financial advice. It requires the advisor to “know their client” deeper than a questionnaire. A risk profile should be seen as a way to facilitate a conversation with your advisor to assess and clarify what type of investor you are, and how much risk you are comfortable with.

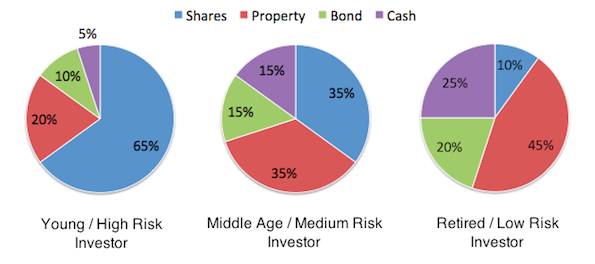

Each of the risk profiles maps to different asset allocations and vary in the split between growth and defensive assets. The varying asset allocations work to adjust the level of volatility and risk for each profile.

- Growth assets include shares or property, and these investments generally have the potential to earn higher returns but carry a higher risk to your capital value over the short-term.

- Defensive assets include fixed interest, bonds, term deposits and cash which provide a lower chance of capital loss but generally lower returns.

Investment Risks Chart

Typical risk profiles and asset allocation ranges are as follows:

- Defensive (10-30% growth assets)

- Conservative (30-50% growth assets)

- Balanced (50-70% growth assets)

- Growth (70-90% growth assets)

- High growth (90-100% growth assets)

If you would like to know more about your own personalised risk profile please feel free to contact us at Oaktreefinancial.ie or call on 025 30588.

Tracy Sumstad is a highly qualified and experienced Senior Financial Consultant with over 20 years of expertise in the Finance Sector. Tracy is well-equipped to provide comprehensive advice on financial planning and corporate solutions. Her focus lies in helping clients identify their unique values and goals, empowering them to make informed financial decisions that protect and enhance their wealth and success.